The United States Social Security Administration (SSA) is an independent agency of the U.S. federal government that administers Social Security, a social insurance program consisting of retirement, disability, and survivors benefits. Social Security is financed through a dedicated payroll tax. Employers and workers each pay 6.2% of wages up to the assessable limit of $137,700 (in 2020), while the independently employed people pay 12.4 %. You are contributing to the Social Security fund over a lifetime of work.

You receive “credits” toward your Social Security while you work and pay Social Security taxes.

The amount of credits that you need to receive retirement benefits depends on your birth date.

If you were born in 1929 or later, 40 credits (10 years of employment) are required. The credits will stay on the Social Security record if you quit working before you have enough credits to apply for benefits. If you go back to work later, you can add more credits to your credentials. Social Security won’t be able to pay any pension benefits until you have the number of credits needed.

Social Security is more than retirement. Most people see Social Security as a system for retirement. Most individuals who get Social Security Benefits are elderly, but some are benefitting because they are:

- Disabled.

- A spouse or child of someone getting benefits.

- A divorced spouse of someone getting or eligible for Social Security.

- A spouse or child of a worker who died.

- A divorced spouse of a worker who died.

- A dependent parent of a worker who died.

You can be eligible for Social Security at any age, depending on your circumstances. Social Security currently provides the children more compensations than any other government program.

Social security benefits replace only some of your earnings when you retire, become disabled, or die. Social Security base the compensation payment on how much you made while employed. Higher earnings over a lifetime result in more significant benefits. If you did not work for a few years or had low incomes, your compensation amount may be smaller than if you were working consistently.

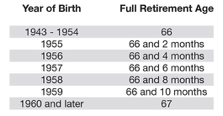

One of the most important choices you will make in your life is choosing when to retire. If you decide to retire when you reach your full retirement age, you will earn the total amount of the payout. When you retire before reaching full retirement age, Social Security will reduce your benefit sum.

IMPORTANT: Although the full retirement age is keep rising, you should still apply for Medicare benefits three months before your 65th birthday. If you wait longer, it can cost you more money to get your Medicare medical benefits (Part B) and prescription drug coverage (Part D).

Related post: Medicare when you are turning 65, where to start?

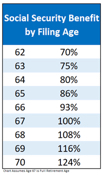

Collecting Social Security Benefits at 62.

You can begin receiving payments as early as 62 years old. They will reduce your benefits if you start early by around half a percent for every month you begin to collect benefits before your full retirement age. For example, if your full retirement age is 66 and 8 months, and you sign up for Social Security when you are 62, then you would get just around 71.7 percent of your full payout.

Delayed Retirement.

Doing what you can to increase your income from social security is a good move if you are worried that you could run out of funds when you retire.

You can decide to keep working past your full retirement age. If you do, you may increase your social security benefits check. Your payout will rise to a certain amount from the time you hit full retirement age, until you begin collecting benefits, or until you turn 70 years old. The percentage varies according to the year you were born.

The maximum monthly Social Security benefit a person may earn per month in 2020 is $3,790 for someone who claims benefits at age 70. The maximum amount is $3,011 for someone at full retirement age and $2,265 for someone at age 62.

How to apply for Social Security?

- You can apply online at www.socialsecurity.gov for retirement benefits.

- You can call toll-free number, 1-800-772-1213 (TTY 1-800-325-0778).

- You can make an appointment and apply in person.

Who is NOT eligible for Social Security Benefits?

Relatively rare, U.S. citizens who worked in the country won’t qualify for Social Security retirement payments. Yet if you’re one of them, you need to know so that you can make sure you have other income streams. Here are some examples:

- People with too few Social Security Credits. (lower than 40)

- Some divorcees.

Occasionally divorced persons can be entitled to half of the Social Security benefits of an ex-spouse. Usually, full-time homemakers or stay-at-home mothers or fathers who weren’t working and therefore didn’t earn profits themselves. Such partners would be at a loss if the marriage lasted less than ten years because they are not entitled to receive Social security payments from the earnings record of their former partner. Only those divorced persons who have been married for more than a decade can claim the benefits of the ex-spouse if they are single, 62 years of age or older, and they will earn fewer smaller amounts based on their records of employment.

- People who die before they reached age 62.

- People who decided to retire abroad.

Generally, you will obtain compensation from the Social Security Administration if you retire in another country. However, some countries are exempt from payments abroad. Azerbaijan, Belarus, Kazakhstan, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, Ukraine, and Uzbekistan.

- Some Government Employees

If a Federal Government hired you before 1984, you might be grandfathered into the Civil Service Retirement System (CSRS). They provide retirement, survivor benefits, and disability. If you one of them, you did not have Social Security taxes withheld from your paycheck. This type of employee may still qualify on other grounds, but the benefit check from Social Security will be reduced.

- Self-employed people who did not file their taxes.

- Some Immigrants over 65.

Retired people who immigrated to the United States won’t have the 40 U.S. credits or ten years of work. They won’t be eligible for Social Security checks. One way to resolve this issue is to gain six job credits in the U.S. and receive prorated U.S. benefits combined with prorated benefits under a totalization agreement from your original country.

I want to add something from my experience with Medicare Beneficiaries in New York.

At First Manhattan Financial, we do a lot of Medicare Planning. We help people apply for Medicare, pick the right Medicare Plan, and guide them through there Medicare journey.

When the Medicare-eligible person does not work and does not collect Social Security Benefits and eligible for it, they must apply for it. When you on the SSA web site filling out the application for Medicare, it does not let you proceed without applying for retirement benefits.

It is important to NOTE that some people may be eligible for SSI. We will cover this topic in another blog.

If you have any questions about your Medicare or retirement, we will be happy to assist. Our dedicated and experienced team can meet with you one on one, conduct phone interviews, or web meeting for your convenience.

1-800-252-7047